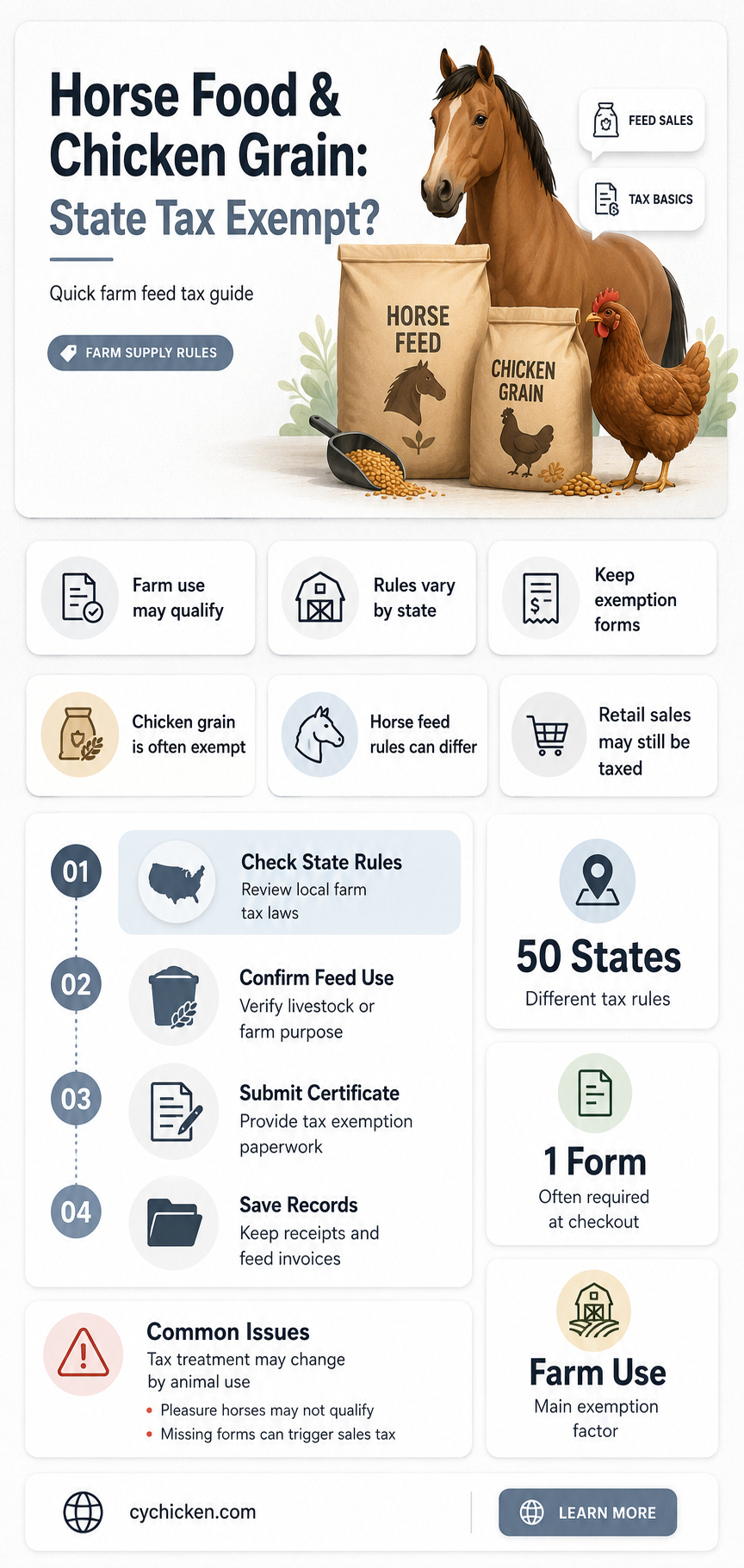

The taxation of food for animals in the United States varies depending on the state and the type of animal. For example, in California, sales of feed for food animals are exempt from tax, whereas feed for non-food animals is generally taxable. In Washington, sales of pharmaceuticals for horses raised by farmers for producing agricultural products for sale are exempt from retail sales tax but are subject to retailing B&O tax. The term food animals does not include horses, and sales of these animals are generally taxable. The Chicken Tax is a term for a 25% tariff on light trucks imported into the US, which was imposed in 1964 in retaliation against European tariffs on American chicken.

| Characteristics | Values |

|---|---|

| Sales tax on horse food | No sales tax on horse food in California and Minnesota |

| Sales tax on chicken grain | No sales tax on chicken grain in California |

Explore related products

What You'll Learn

- Sales of horse food and chicken grain are generally not taxable if they are for food animals

- Sales of feed for non-food animals are taxable, with some exceptions

- Tax does not apply to sales of medicated feed for food or non-food animals

- Sales of feed in small units (two standard sacks of grain or less) are usually exempt from tax

- Sales of feed for breeding animals whose offspring will be sold are exempt from tax

![]()

Sales of horse food and chicken grain are generally not taxable if they are for food animals

In the context of feed for food animals, grain is specifically mentioned as a type of feed that is typically exempt from sales tax. This exemption applies when the feed is of a kind ordinarily used only in the production of meat, dairy, or poultry products for human consumption. Small quantities of feed, such as two standard sacks of grain or less, and four bales of hay or less, are also presumed to be exempt from tax.

Additionally, medicated feed, which is used for the prevention and control of diseases in food animals, is also exempt from sales tax. This exemption extends to the ingredients purchased by a buyer who mixes them to create an exempt medicated feed rather than a drug. However, drugs or medicines administered to non-food animals, including racehorses, are generally subject to tax.

It is worth noting that the taxation of feed and animals can vary depending on the state and specific circumstances. For example, in California, the sale of animals that do not meet the definition of food animals is taxable, regardless of their use. On the other hand, in Minnesota, all horses, including racehorses, working stock, or pets, are exempt from sales tax, and related items and services consumed in horse-related activities are also exempt.

Farmers and ranchers may also be eligible for various tax credits and benefits, such as the Fuel Excise Tax Credit and Solar Energy Credits, depending on the nature of their farming business and the state they live in. Therefore, it is essential to refer to the specific laws and regulations of each state to understand the taxation rules applicable to the sale of horse food and chicken grain.

Chicken Temperature: Where to Measure?

You may want to see also

Explore related products

![]()

Sales of feed for non-food animals are taxable, with some exceptions

Sales of feed for non-food animals are generally taxable. However, there are some exceptions to this rule.

Firstly, it is important to understand what constitutes "feed." Feed includes grain, hay, seed, kibble, and similar products. Some feed, like alfalfa, can be used for both food and non-food animals.

Now, let's clarify the difference between food and non-food animals. Food animals are those commonly used in producing food or intended for human consumption, such as cattle, sheep, swine, baby chicks, hatching eggs, fish, bees, and rabbits. On the other hand, non-food animals are those not typically consumed by humans and may include pets or companion animals, such as cats, dogs, horses, mink, and canaries.

With that distinction in mind, we can now explore the exceptions to the taxation of feed for non-food animals:

- Medicated Feed: Tax does not apply to the sale of medicated feed used for the prevention and control of diseases in non-food animals that are to be sold in the regular course of business.

- Ingredients for Medicated Feed: Tax exemption also applies when a purchaser acquires the individual ingredients for mixing their medicated feed, provided that the final product is an exempt medicated feed rather than a drug.

- Feed for Animals Sold in Business Operations: Feed sold for non-food animals that will be sold as part of the purchaser's business operations is exempt from tax. For example, kibble for puppies at a pet store or bone meal for bird breeders who sell the chicks.

- Feed for Breeding Animals: Feed sold for breeding animals whose offspring will be sold in the purchaser's business operations is also exempt from tax.

- Small Quantity Exemptions: In some states, sales of small quantities of feed, such as two standard sacks of grain or less and/or four bales of hay or less, may be exempt from tax, regardless of whether they are for food or non-food animals.

- Labeling and Presumptions: Feed that bears a manufacturer's label indicating that it is intended for food animals is generally exempt from tax. Additionally, in the absence of evidence to the contrary, it is presumed that sellers of feed ordinarily used in producing meat, dairy, or poultry products for human consumption are making exempt sales.

It is important to note that these exceptions may vary by state, and specific regulations and requirements should be consulted for each jurisdiction.

Chicken Marsala Carbs: Olive Garden's Secret

You may want to see also

Explore related products

![]()

Tax does not apply to sales of medicated feed for food or non-food animals

The sale of medicated feed for food or non-food animals is exempt from tax. Medicated feed is defined as feed that includes items such as cod liver oil, salt, bone meal, calcium carbonate, double-purpose limestone, granulars, and oyster shells. It does not include sand, charcoal, granite grit, sulphur, and medicines. The primary purpose of medicated feed is the prevention and control of disease in food or non-food animals that are to be sold in the regular course of business.

This means that the sale of medicated feed for horses and chickens is also exempt from tax, as these animals are considered food animals. Food animals are defined as any form of animal life whose products ordinarily constitute food for human consumption. This includes cattle, sheep, swine, baby chicks, hatching eggs, fish, bees, and rabbits. The sale of racehorses, for example, is generally taxable, but the feed used for these animals is not.

The exemption also applies to sales in small units of feed, such as two standard sacks of grain or less, and four bales of hay or less. This feed is typically used for food production or other purposes, such as feeding work stock. It also applies to sales of feed that is specifically labeled by the manufacturer for food animals.

Additionally, the sale of drugs or medicines administered directly to food animals is exempt from tax. This includes drugs or medicines that are approved by the United States Food and Drug Administration (FDA) and are defined and registered pursuant to the relevant sections of the California Food and Agricultural Code. However, the sale of drugs or medicines administered directly to non-food animals is subject to tax, regardless of whether these animals are being held for sale.

It is important to note that the information provided here is based on the regulations outlined by the California Department of Tax and Fee Administration (CDTFA) and may not apply to other states or countries.

Brining Chicken: Is It Worth the Salt?

You may want to see also

Explore related products

![Feed (2005) [Limited Edition]](https://m.media-amazon.com/images/I/714xIrFTCJL._AC_UY218_.jpg)

![]()

Sales of feed in small units (two standard sacks of grain or less) are usually exempt from tax

In California, for example, tax does not apply to sales of feed for food animals. However, feed sold for a non-food animal is generally taxable. There are two exceptions to this rule: if the feed is sold for the purpose of feeding animals that will be sold in the purchaser's business operations, or to feed breeding animals whose offspring will be sold in the purchaser's business operations.

In Minnesota, all horses are exempt from sales tax, including racehorses, working stock, or pets. Related items and services are also not taxable if used or consumed in breeding, boarding, keeping, owning, and raising horses.

It is important to note that the tax rules for feed may vary by state and specific circumstances. For example, in California, ground manure sold to chicken raisers and spread in chicken houses as litter, which is partially consumed by the chickens, does not qualify as exempt feed.

McDonald's Crispy Buttermilk Chicken Tenders: Carb Count

You may want to see also

Explore related products

![]()

Sales of feed for breeding animals whose offspring will be sold are exempt from tax

In California, all sales are taxable unless the law provides a specific exemption. Sales of feed for breeding animals whose offspring will be sold as part of business operations are exempt from tax. This exemption applies to feed ordinarily used only in the production of meat, dairy, or poultry products for human consumption. It includes two or fewer standard sacks of grain, four or fewer bales of hay, or both. Feed bearing a manufacturer's label indicating that it is intended for food animals is also exempt.

Feed sold for non-food animals is generally taxable. However, there are two exceptions. Feed is exempt from tax if it is sold for the following purposes:

- To feed animals that will be sold in the purchaser's business operations, such as kibble for puppies at a pet store.

- To feed breeding animals whose offspring will be sold in the purchaser's business operations, such as bone meal for bird breeders who sell the chicks.

It is important to note that facilities that charge a flat fee for boarding services, including feed consumed, are responsible for paying the tax on the feed they purchase. Additionally, sales of feed for racehorses are subject to tax.

In Minnesota, sales of feed, feed additives, and feed supplements for agricultural animals are not taxable. However, feed for other animals may be taxable.

Chicken Protein Power: Grams Per Serving

You may want to see also